|

Provided to you Exclusively By Bob Bednarz |

For the week of Jul 07, 2025 | Vol. 23, Issue 27 |

|

Bob Bednarz

Loan Advisor NMLS ID 259771 Guarantee Mortgage is a Division of American Pacific Mortgage Corporation NMLS #1850 Cell: 415-871-5756 Direct: 415-891-3405 Efax: 415-329-1951 E-Mail: bbednarz@guaranteemortgage.com Website: www.guaranteemortgage.com |

|

| A Look Into the Markets |

The 4th of July marks the birth of our nation's independence, a day to celebrate the freedom and opportunity that define America. We honor the sacrifices of those who fought for our liberty, gathering with family and friends under starlit skies to reflect on the values that unite us. This holiday is a reminder of our nation's strength, built on unity and a shared commitment to progress. Let us celebrate with gratitude and dedication to America's enduring principles. "America, sweet America. You know, God done shed His grace on thee. He crowned thy good, yes, He did, in brotherhood. From sea to shining sea" America the Beautiful by Ray Charles Stocks Reach New Highs This past week, interest rates dropped to their lowest level since early April. While bonds have enjoyed a strong rally over the past several weeks, stocks have also surged, hitting all-time highs. Positive developments in Israel-Iran relations and the passage of a significant bill through Congress have fueled this upward momentum. However, this dynamic where stocks rise while interest rates fall, is not sustainable indefinitely. On Tuesday, a bearish technical signal emerged in the bond market, suggesting that the recent rally in bonds may be pausing or nearing its end. Refer to the chart section below for a detailed look at what transpired. Pressure on Powell Federal Reserve Chair Jerome Powell has faced criticism for maintaining high interest rates amid disinflation and low energy prices. In a recent speech, Powell noted that he would have cut rates sooner if not for concerns about tariffs. While it remains uncertain whether tariffs will significantly impact prices and inflation, many Fed members have acknowledged that tariff-related price pressures have not yet materialized. With the 90-day tariff relaxation period ending on July 9, the market will soon see if tariffs drive inflation higher. Labor Market Holding Steady A forward-looking labor market report showed a substantial increase in job openings in May, exceeding expectations. Additionally, last week's initial unemployment claims came in lower than anticipated. Currently, the labor market is stable, with neither significant layoffs nor robust hiring. The passage of the significant bill may bring clarity on taxes and regulations, potentially influencing hiring trends. 30-Year Mortgage Rates The 30-year fixed rate mortgage averaged 6.69% as of July 2, 2025, down from last week when it averaged 6.77%. 4.20% The 10-year Treasury note, which closely correlates with mortgage rates, traded at a critical level of 4.20% before the bearish technical signal emerged. For mortgage rates to continue their downward trend, the 10-year note must decisively fall beneath 4.20% and sustain that level. The bond market and interest rates have benefited from a nice rally in prices and decline in rates. However, this trend may be pausing or reversing. Housing and mortgage professionals, along with their clients, should closely monitor these key levels, particularly the 4.20% threshold mentioned above. Looking Ahead Next week features a lighter economic data calendar, but several events could move markets. The release of the minutes from the previous Federal Reserve meeting will provide insight into how members view the economy, inflation, and the future direction of interest rates. Additionally, markets will watch for the passage of the significant bill through Congress and its potential impact on bonds and rates. Finally, the expiration of the 90-day tariff pause on July 9 will reveal whether tariffs affect prices and inflation, which has not been a major concern thus far. |

| Economic Calendar |

|

As noted earlier, a bearish technical signal appeared last Tuesday, known as a bearish engulfing pattern, a concept rooted in Japanese candlestick charting developed by rice traders centuries ago. Here's the psychology: on Tuesday, bond prices opened significantly above Monday's close, with rates dropping further. However, prices then fell, closing below the previous day's close, forming a candlestick that "engulfs" the prior day's candle. This pattern, occurring at the end of a rally and at a key technical level, is a classic reversal signal that should not be ignored. For rates to improve, bond prices must push higher, surpassing the large red candlestick on the far right of the chart. If they fail to do so, optimism for lower rates in the near term should be tempered. Chart: Fannie Mae Mortgage Bond (Friday July 4, 2025)

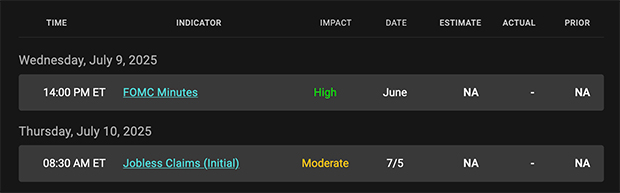

Economic Calendar for the Week of July 7 - 11  |

|

Bob Bednarz

Guarantee Mortgage 300 Tamal Plaza, Suite 250 Corte Madera, CA 94925  |