|

Provided to you Exclusively by Rick Phillips |

For the week of Jun 23, 2025 | Vol. 23, Issue 25 |

|

Rick Phillips

Loan Officer NMLS ID # 614072 First United Mortgage Group Office: 281-367-0904 Cell: 713-419-9012 E-Mail: rphillips@firstunitedbank.com Website: www.RickCPhillips.com |

|

| A Look Into the Markets |

This past week, interest rates held steady despite the Fed not cutting and forecasting higher rates for longer. Let's review what happened and look at the week ahead. "At first, I was afraid, I was petrified. Thinking I could live without you by my side. And after spending nights. Thinking how you did me wrong. I grew strong. And I learned how to get along". I Will Survive - Gloria Gaynor "Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated." FOMC Statement, June 18, 2025. Fed Holds Rates Steady As noted in the quote above, the Federal Reserve maintained the Fed Funds Rate (overnight lending rate) at a target range of 4.25% to 4.50%. This rate does not directly impact mortgage rates but affects short-term loans like auto loans, credit cards, and home equity lines of credit. This move was widely expected, but the updated Summary of Economic Projections surprised markets. Here's the breakdown:

Over the last 90 days, the Fed now anticipates slightly higher unemployment and lower economic growth (GDP). The big surprise was a significant jump in projected inflation for the second half of 2025. This is why the Fed isn't cutting rates today and may only cut twice this year and once annually for the next two years. In the press conference, Fed Chair Powell noted that "goods inflation" is expected this summer, with tariffs likely increasing costs for consumers. He also admitted, "It is very hard to measure what is going on in the economy," highlighting uncertainty about the economy's direction. The punchline: This forecast and stance on rates and inflation could shift significantly by the next update, especially once tariffs take effect on July 9. Keep an eye on that date and its economic impact. Homebuilder Sentiment Homebuilder confidence is down, with the builder sentiment index dropping to its third-lowest level since 2012. "Buyers are increasingly moving to the sidelines due to elevated mortgage rates and tariff and economic uncertainty," said NAHB Chairman Buddy Hughes. This sums it up: homebuilders are grappling with uncertainty around tariffs and persistently high mortgage rates. Some Labor Market Weakness Initial and Continued Claims, key indicators of labor market health, have edged higher in recent weeks, signaling some weakness. The Fed has previously noted that "any further cooling in the labor market would be unwelcome." Despite Powell downplaying massive layoffs, Microsoft recently announced thousands of job cuts, including many in sales. If labor market conditions worsen, the Fed may reconsider its stance on rates. 30-Year Mortgage Rates The 30-year fixed rate mortgage averaged 6.81% as of June 18, 2025, down from the previous week when it averaged 6.84%. 4.50% as a Key Level The 4.50% yield on the 10-year Treasury note has acted as a ceiling in the bond market, preventing rates from rising higher over the past month. If this level holds, it could cap rate increases. However, if inflation cools and bond demand remains strong, rates could trend lower. Bottom Line: Uncertainty persists regarding the economy and interest rates. Clarity on tariffs and fiscal policy, including the "Big Beautiful Bill," will provide a better sense of where rates are headed. Looking Ahead Next week is packed with key data. The Fed's preferred inflation gauge, Core PCE, will be released, with May's year-over-year inflation expected at 2.6%, nearing the Fed's 2.0% target. We'll also get a GDP reading on economic growth. Additionally, the Treasury will auction $183 billion in new debt, which could move markets. |

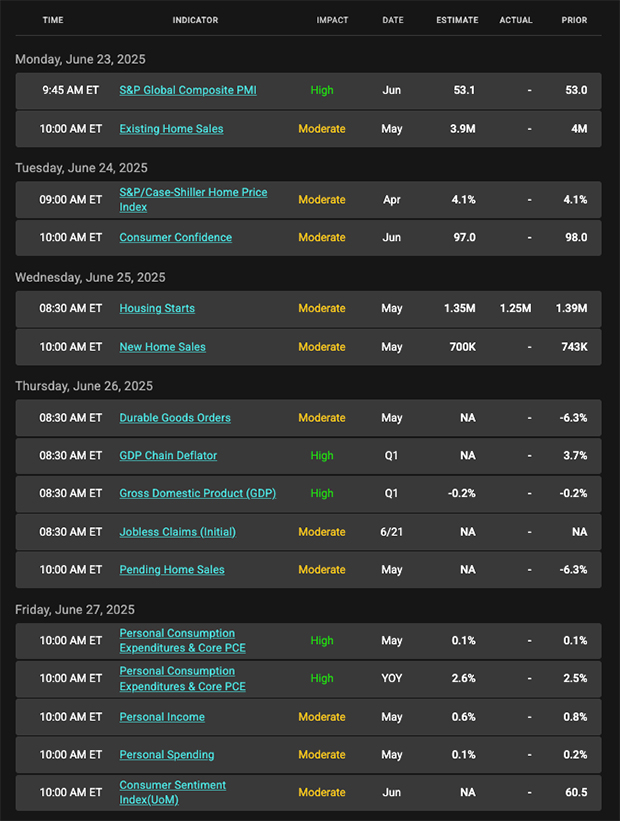

| Economic Calendar |

|

For homebuyers and refinancers, mortgage rates are closely tied to mortgage bond prices. The chart below tracks the Fannie Mae 30-year 6.0% coupon. The rule is simple: rising bond prices mean lower mortgage rates, while falling prices push rates higher. The right side of the chart shows prices rising after lower-than-expected inflation data. For rates to drop further, the bond price needs to break above $101.50, a level it hasn't consistently reached in over eight months. Chart: Fannie Mae Mortgage Bond (Friday June 20, 2025)

Economic Calendar for the Week of June 23 - 27  |

|

Rick Phillips

First United Bank Mortgage Group 9400 Grogans Mill, Ste 205 The Woodlands, TX 77380  |